Dreaming of a kitchen remodel, a luxurious bathroom, or a backyard oasis? Home improvement projects can transform your living space, but financing can be a hurdle. Thankfully, Wells Fargo offers a range of solutions to help you turn those dreams into reality. In this article, we’ll explore the various Wells Fargo financing options specifically designed for home improvements, helping you choose the right solution for your needs and budget.

Toc

- 1. Understanding Wells Fargo Financing Home Improvement

- 2. Factors to Consider When Choosing Wells Fargo Financing

- 3. Related articles 01:

- 4. Alternatives to Wells Fargo Financing

- 5. Mastering the Art of Managing Your Wells Fargo Home Financing

- 6. Related articles 02:

- 7. FAQ: Answering Your Burning Questions

- 8. Conclusion: Unlock Your Dream Home with Wells Fargo Financing

Understanding Wells Fargo Financing Home Improvement

Wells Fargo understands that home renovations can be a significant investment, and they’ve designed their financing options to cater to the unique needs of homeowners like you.

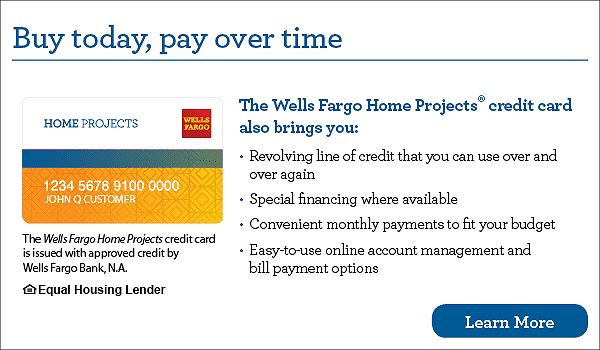

Wells Fargo Home Projects® Credit Card: Your Renovation Companion

The Wells Fargo Home Projects® Credit Card is a financing tool tailored for home improvement enthusiasts. Its standout feature is the convenience of monthly payments, which can be a lifesaver when budgeting for larger-scale projects.

The most appealing aspect? Those enticing 0% APR promotional financing periods that allow you to tackle your renovations without immediate interest charges. Imagine the joy of upgrading your kitchen or revamping your bathroom without breaking the bank. Plus, the easy online account management makes it a breeze to track your expenses.

However, it’s important to note that the card does come with a high APR for regular purchases. If you don’t pay off the balance during the promotional period, those interest charges can quickly start to add up. Additionally, the card’s acceptance is limited to participating home improvement stores, which might restrict your options.

Unleashing the Power of a Wells Fargo Home Equity Line of Credit (HELOC)

If you’ve built up a healthy amount of home equity, a Wells Fargo Home Equity Line of Credit (HELOC) could be the perfect financing solution for your home improvement plans. Compared to traditional credit cards, HELOCs typically offer lower interest rates, making them a more cost-effective choice.

The flexibility of a HELOC is a major perk. You can draw funds as needed, using the equity in your home to your advantage. This means you can start your project without having to wait for all the funds to be available upfront. However, keep in mind that qualifying for a HELOC requires a decent amount of home equity, which might not be accessible to all homeowners. Additionally, the variable interest rates can lead to unexpected changes in your monthly payments, so it’s essential to manage your HELOC carefully.

Wells Fargo Home Improvement Loans: Predictable Payments, Endless Possibilities

Another option in Wells Fargo’s home financing arsenal is the Home Improvement Loan. These loans provide a lump sum of funds that you can use for a wide range of projects, from kitchen renovations to roof replacements.

The standout feature of Wells Fargo Home Improvement Loans is the fixed interest rate, which translates to predictable monthly payments. This can be a welcome relief, especially for those tackling larger-scale endeavors. And the best part? The interest you pay on these loans may even be tax-deductible, adding an extra layer of financial benefit.

It’s worth noting that these loans do require a credit check and income verification, and they may come with higher interest rates compared to HELOCs. There could also be closing costs involved, so be sure to factor those into your budget.

Factors to Consider When Choosing Wells Fargo Financing

When selecting the right Wells Fargo financing option for your home improvement project, there are several key factors to keep in mind.

Credit Score: The Gateway to Favorable Terms

Your credit score plays a pivotal role in determining your eligibility for Wells Fargo’s home financing products. As a general rule, the higher your credit score, the better the interest rates and terms you’ll qualify for.

If your credit score needs a little work, now’s the time to take steps to improve it. Pay down existing debts, correct any inaccuracies on your credit report, and keep an eye on your utilization ratio. Doing so can open the door to more favorable financing conditions and help you save a significant amount of money in the long run.

Interest Rates and APR: The Numbers That Matter

Understanding the nuances of interest rates and APR (Annual Percentage Rate) is essential when selecting a Wells Fargo financing option. Fixed-rate loans offer stability, while variable-rate options can fluctuate, potentially increasing your costs over time.

When comparing offers, pay close attention to the interest rates and APR. A lower APR means you’ll pay less in interest over the life of the loan, so it’s worth taking the time to shop around and find the most competitive rates.

1. https://viralblogspost.com/local-roofing-companies-that-finance

2. https://viralblogspost.com/mmoga-newtek-small-business-finance

3. https://viralblogspost.com/mmoga-master-of-science-in-finance

4. https://viralblogspost.com/mmoga-roofing-companies-that-finance

For instance, if you’re considering a Home Improvement Loan, a fixed rate might give you peace of mind, knowing that your payments won’t suddenly spike due to interest rate changes. Conversely, a HELOC with a variable rate could be beneficial if you anticipate paying off the balance quickly, but it does come with its own set of risks.

Repayment Terms: Balancing Monthly Budgets and Long-Term Savings

The repayment terms of your Wells Fargo financing can have a significant impact on your monthly cash flow and overall financial well-being. Consider whether you prefer fixed monthly payments or interest-only options, and weigh the trade-offs between a shorter loan term (higher payments, lower interest costs) and a longer term (lower payments, higher interest costs).

Striking the right balance between your current budget and long-term savings goals is crucial. Don’t be afraid to crunch the numbers and explore different scenarios to find the solution that fits your needs best. For example, a shorter loan term might be more appealing if you can manage higher monthly payments, allowing you to save on interest over time.

Alternatives to Wells Fargo Financing

While Wells Fargo offers a robust suite of home financing options, it’s always wise to explore alternative solutions that might better suit your unique circumstances.

Home Improvement Loans from Other Lenders

Look beyond Wells Fargo and consider home improvement loans from credit unions, online lenders, and local banks. These institutions often provide competitive interest rates and may have more flexible eligibility criteria. It’s worth your time to shop around and compare offers to find the best deal.

For instance, some credit unions have been known to offer lower rates and personalized service compared to larger banks. Additionally, online lenders may provide a more streamlined application process, allowing you to secure funds quickly for your project.

Government-Backed Loan Programs

Homeowners might also want to explore government-backed loan programs, such as the FHA 203(k) loan or the USDA Section 504 loan. These options can be particularly helpful for those who may not qualify for traditional financing, as they often come with lower down payment requirements and more lenient credit score standards.

The FHA 203(k) loan, for example, allows you to borrow money for both purchasing a home and renovating it. This can be a game-changer for first-time homebuyers who may need to make significant repairs before moving in.

Home Equity Loans: A Lump-Sum Solution

If you’ve built up a significant amount of home equity, a home equity loan could be a viable alternative to Wells Fargo’s financing options. These loans provide a lump sum of money based on the equity in your home, which you can then use for your renovation projects. Just be sure to carefully weigh the risks, as a home equity loan uses your home as collateral.

For larger projects, a home equity loan can be a good fit, especially if you prefer a fixed interest rate and predictable monthly payments. However, it’s crucial to assess your financial situation and make sure you can handle the added debt.

Mastering the Art of Managing Your Wells Fargo Home Financing

Effective management of your Wells Fargo home financing is crucial to maintaining financial stability and ensuring the success of your home improvement projects.

Budgeting and Payment Planning: The Key to Staying on Track

Creating a detailed budget is essential when embarking on any home renovation journey. Track your expenses meticulously, and set up automatic payments to avoid late fees and ensure timely repayment. By staying on top of your finances, you can avoid unnecessary headaches and focus on bringing your vision to life.

Consider using budgeting tools or apps that can help you monitor your spending in real-time. These tools can provide insights into where your money is going and help you adjust your budget as needed.

Credit Monitoring: Safeguarding Your Financial Future

Regularly monitoring your credit score is a must-do when leveraging Wells Fargo financing options. Keep a close eye on your credit report and dispute any errors you find. Maintaining a healthy credit profile can open the door to more favorable terms and better interest rates in the future.

Sign up for credit monitoring services that alert you to changes in your credit report. This proactive approach can help you catch any issues early, allowing you to address them before they impact your financing options.

Keeping Communication Open with Wells Fargo

Don’t underestimate the importance of maintaining communication with your Wells Fargo representative. If you have questions or concerns about your financing options, reach out for clarification. They can provide insights tailored to your specific situation and help you navigate the complexities of your home improvement financing.

1. https://viralblogspost.com/mmoga-master-of-science-in-finance

2. https://viralblogspost.com/how-a-personal-loan-can-help-you-pay-off-credit-card-debt

3. https://viralblogspost.com/mmoga-masters-in-finance-vs-mba

4. https://viralblogspost.com/mmoga-online-masters-in-finance

Additionally, if you encounter financial challenges during your project, don’t hesitate to discuss your options with Wells Fargo. They may offer solutions such as restructuring your loan or providing temporary relief.

FAQ: Answering Your Burning Questions

Q1: What are the minimum credit score requirements for Wells Fargo home improvement financing?

A: The credit score requirements vary depending on the specific financing option. It’s best to contact Wells Fargo directly to get the most up-to-date information on their eligibility criteria.

Q2: What are the closing costs associated with Wells Fargo home improvement loans?

A: The closing costs can vary depending on the loan type and amount. It’s essential to reach out to Wells Fargo to get the details on the specific closing costs for your situation.

Q3: Can I use Wells Fargo financing for both home purchase and renovation?

A: Yes, Wells Fargo offers programs like the FHA 203(k) loan that combine home purchase and renovation financing.

Q4: How can I check my eligibility for Wells Fargo home improvement financing?

A: You can use Wells Fargo’s online pre-qualification tool or speak with a Wells Fargo loan officer to determine your eligibility.

Q5: What are the benefits of using Wells Fargo financing for home improvement projects?

A: Wells Fargo offers a range of benefits, including convenient monthly payments, flexible financing options, and easy online account management.

Conclusion: Unlock Your Dream Home with Wells Fargo Financing

Wells Fargo provides a diverse range of financing options tailored to meet the unique needs of homeowners undertaking home improvement projects. By carefully considering your credit score, interest rates, repayment terms, and alternative financing options, you can choose the solution that best aligns with your financial goals and project scope.

Whether you opt for their Home Projects® Credit Card, a HELOC, or a Home Improvement Loan, each option presents its own advantages and considerations. By taking the time to explore these choices and manage your financing effectively, you’ll be well on your way to transforming your dream home into a reality.

So, what are you waiting for? Contact Wells Fargo today to discuss your home improvement financing needs and let them help you unlock the door to your dream home.

Leave a Reply