Imagine a world where you don’t have to wait weeks for customer payments, freeing up cash to invest in growth, hire new talent, or simply cover operational expenses. This is the power of accounts receivable financing factoring, a financial strategy that can be a game-changer for small businesses facing cash flow challenges.

Toc

In this article, we’ll guide you through the ins and outs of accounts receivable financing factoring, explaining how it works, its benefits, and how to choose the right factoring solution for your unique needs.

Understanding Accounts Receivable Financing Factoring

What is Accounts Receivable Financing Factoring?

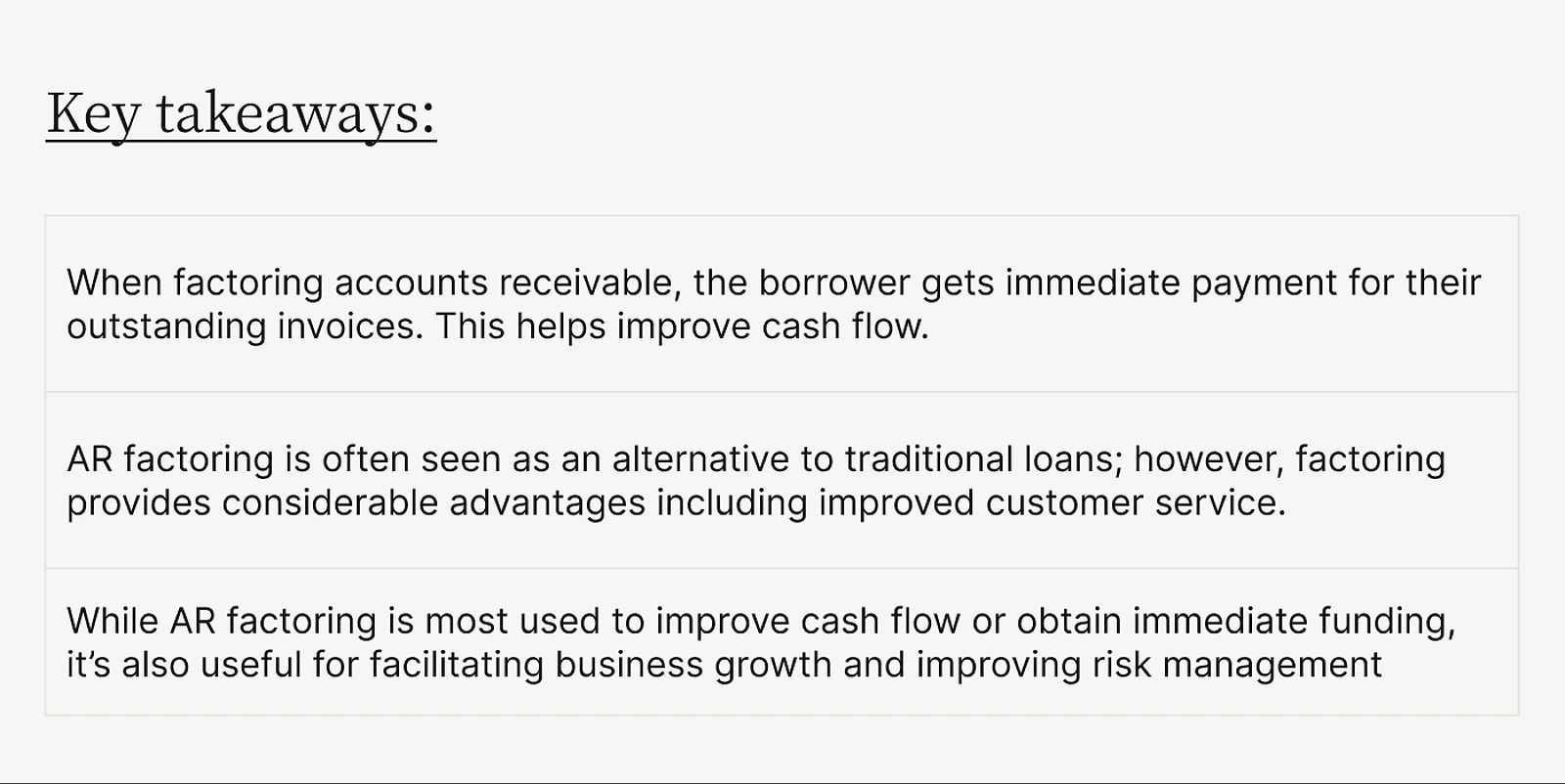

Accounts receivable financing factoring is a financial strategy where businesses sell their unpaid invoices to a third-party factoring company at a discount for immediate cash. This process allows you to convert your outstanding invoices into immediate cash flow, bypassing the often lengthy wait for customer payments.

The factoring company will evaluate the creditworthiness of your customers and provide you with a lump-sum payment, typically ranging from 70% to 90% of the invoice value. Once the customer pays the invoice, the factoring company collects the full amount and remits the remaining balance to you, minus the discount rate.

How Does Accounts Receivable Financing Factoring Work?

The accounts receivable financing factoring process typically involves the following steps:

- You submit your invoices to the factoring company for review.

- The factoring company assesses the creditworthiness of your customers and determines the appropriate discount rate.

- The factoring company provides you with an advance payment, usually between 70% and 90% of the invoice value.

- The factoring company collects the full invoice amount from your customer.

- Once the customer pays, the factoring company remits the remaining balance to you, minus the discount rate.

Factoring vs- Traditional Loans

When comparing accounts receivable financing factoring to traditional bank loans, there are several key differences:

- Eligibility: Factoring is generally more accessible, particularly for small businesses with limited credit histories. Traditional loans often require a solid credit score and a proven track record.

- Approval Process: The approval process for factoring can be completed in just a few days, whereas traditional loans may take weeks or even months to secure.

- Interest Rates: While factoring typically has higher rates than traditional loans, the immediate cash flow it provides can outweigh the costs for small businesses facing urgent financial needs.

- Collateral Requirements: Unlike many bank loans, factoring does not require collateral, making it a favorable option for small businesses with few tangible assets.

Benefits of Accounts Receivable Financing Factoring for Small Businesses

Improved Cash Flow Management

Cash flow is the lifeblood of any small business, and accounts receivable financing factoring offers a way to manage it effectively. By converting outstanding invoices into immediate cash, you can:

- Cover Operational Expenses: The cash generated from factoring can be used for payroll, rent, and other essential costs.

- Seize New Opportunities: With a steady cash flow, you can invest in marketing campaigns, new projects, or equipment without the stress of waiting for customer payments.

- Enhance Business Stability: Improved cash flow reduces the risk of financial distress, allowing you to focus on growth rather than survival.

Funding for Growth and Expansion

Accounts receivable financing factoring is not just about immediate cash; it also provides a crucial avenue for funding growth initiatives. You can utilize the cash from factoring to:

- Hire New Talent: As your business expands, hiring skilled employees becomes essential. Factoring can provide the necessary funds to attract and retain top talent.

- Enter New Markets: Cash flow from factoring can support market research and entry strategies, allowing you to diversify and grow your customer base.

- Develop New Products: Innovating and launching new products requires funding. Factoring can help cover research and development costs.

Access to Capital Without Collateral

For many small businesses, traditional financing options can be daunting due to a lack of collateral. Accounts receivable financing factoring allows you to access capital without putting your assets at risk. This is particularly beneficial if you don’t have substantial physical assets to offer as security.

- Risk Mitigation: Factoring provides a way to secure funding without jeopardizing personal or business assets, enabling you to focus on growth without the pressure of collateral requirements.

- Financial Flexibility: You can manage your cash flow more effectively, allowing you to pivot or adapt to changing market conditions without the constraints of traditional financing.

Flexibility and Convenience

Accounts receivable financing factoring offers a level of flexibility that resonates well with small businesses. The ability to choose which invoices to factor allows you to:

- Control Cash Flow: You can decide how much cash you need at any given time, tailoring your financing strategy to your current financial situation.

- Simplified Application Process: The application process for factoring is typically more straightforward than that of traditional loans, which can involve extensive documentation and lengthy approvals.

Finding the Right Accounts Receivable Financing Factoring Solution

Factors to Consider When Choosing a Factoring Company

Selecting the right factoring company is crucial for maximizing the benefits of accounts receivable financing factoring. When evaluating potential providers, consider the following factors:

- Discount Rates and Fees: Compare the costs associated with different factoring companies to find the most favorable terms.

- Advance Rates: Look for companies that offer competitive advance rates, allowing you to access a larger percentage of your invoices upfront.

- Creditworthiness of Customers: Understanding the credit profiles of your customers can impact the terms you receive from factoring companies.

- Reputation and Experience: Research the reputation and track record of factoring companies, especially their experience within your industry.

- Customer Service and Support: A responsive and helpful factoring company can make the process smoother and more beneficial for your business.

Negotiating the Best Terms

As a small business owner, don’t hesitate to negotiate with factoring companies to secure favorable terms. Here are some tips:

- Shop Around: Compare quotes from multiple companies to identify the best rates and terms.

- Negotiate Higher Advance Rates: Don’t be afraid to ask for better advance rates or explore the possibility of non-recourse factoring.

- Understand the Agreement: Ensure you fully comprehend the terms and conditions of the factoring agreement before signing.

Evaluating the Costs and Benefits

To determine if accounts receivable financing factoring is the right solution for your small business, carefully evaluate the costs and benefits. This involves:

- Calculating Total Costs: Assess the total cost of factoring, including discount rates, fees, and any additional expenses.

- Weighing Immediate Cash Flow: Consider the benefits of immediate cash flow against the costs of factoring to make an informed decision.

- Exploring Alternative Financing Options: Investigate other financing avenues, such as business lines of credit or equity financing, to ensure you choose the most suitable path for your needs.

By carefully considering these factors, you can find the right accounts receivable financing factoring solution to unlock your business’s cash flow potential and fuel its growth.

Additional Considerations

Types of Accounts Receivable Financing Factoring

There are several types of accounts receivable financing factoring, each with its own unique characteristics:

-

Recourse Factoring: In this type of factoring, the small business retains responsibility for unpaid invoices even after selling them to the factoring company. If a customer fails to pay, the factoring company can require the small business to buy back the invoice or refund the advance payment. Recourse factoring typically comes with lower discount rates, making it an attractive option for small businesses with strong customer relationships and a low risk of non-payment.

-

Non-Recourse Factoring: Non-recourse factoring shifts the risk of non-payment from the small business to the factoring company. If a customer does not pay the invoice, the factoring company absorbs the loss. While this option provides greater security for the small business, it typically comes with higher discount rates due to the increased risk for the factoring company.

-

Spot Factoring: Spot factoring allows small businesses to sell a single invoice to a factoring company rather than entering into a long-term agreement. This option is particularly useful for businesses that experience intermittent cash flow challenges, providing immediate cash without a commitment to ongoing factoring services.

-

Maturity Factoring: Maturity factoring is less common and involves the factoring company advancing payment on an invoice and collecting payments from the small business as the invoice matures. This arrangement is generally used for larger contracts or invoices with longer payment cycles, offering small businesses a way to manage cash flow over an extended period.

1. https://viralblogspost.com/archive/3436/

2. https://viralblogspost.com/archive/3631/

3. https://viralblogspost.com/archive/3466/

Tips for Success with Accounts Receivable Financing Factoring

To maximize the benefits of accounts receivable financing factoring, consider the following best practices:

- Maintain Accurate Records: Keeping up-to-date records of invoices is crucial for smooth transactions with factoring companies.

- Assess Customer Creditworthiness: Ensure that your customers have a history of timely payments to reduce the risk of non-payment.

- Communicate Effectively: Establish clear communication with your factoring company to enhance the relationship and streamline processes.

- Monitor Cash Flow: Regularly track your cash flow and manage expenses to leverage factoring strategically for growth.

By understanding the different types of factoring and implementing these best practices, you can maximize the benefits of accounts receivable financing factoring and unlock your small business’s full potential.

FAQ

What is the typical discount rate for accounts receivable financing factoring?

Discount rates can vary widely based on factors such as customer creditworthiness, invoice terms, and the risk appetite of the factoring company. Rates typically range from 1% to 5% per month.

What are the risks associated with accounts receivable financing factoring?

The primary risk is that the factoring company may not be able to collect payment from your customers, resulting in a loss for you. This risk is mitigated with non-recourse factoring, where the factoring company assumes the risk of non-payment.

How can I find a reputable accounts receivable financing factoring company?

Research online reviews, industry associations, and financial publications to identify reputable factoring companies. Additionally, consider seeking recommendations from other small business owners or business advisors.

1. https://viralblogspost.com/archive/3096/

2. https://viralblogspost.com/archive/3368/

3. https://viralblogspost.com/archive/3319/

Leave a Reply