If you’ve recently married or welcomed a new addition to the family, it’s a good time to consider life insurance. Review your current coverage to ensure it meets your needs. Life insurance is a key aspect of financial security that requires attention. While it may seem complex or dull, it plays a vital role in safeguarding your loved ones’ future. Once someone depends on you financially, especially a child or spouse, having life insurance is crucial. Acting sooner rather than later is advisable, as coverage is more affordable for young and healthy individuals.

Toc

- 1. How to buy life insurance

- 2. What kind of life insurance to buy

- 3. Where to get online life insurance quotes

- 4. Related articles 01:

- 5. Information you need to get your quote

- 5.1. You’ll complete a brief form about you

- 5.2. Select how much insurance you need (and for how long)

- 5.3. You may be surprised to see a wide range of prices from different insurers

- 5.4. Learn your class: preferred, super-preferred, standard, or substandard

- 5.5. Compare quotes from over a dozen insurance carriers

- 6. How to apply for a life insurance policy

- 7. Related articles 02:

- 8. What to expect after you apply

- 9. Conclusion

How to buy life insurance

There are three fundamental approaches to purchasing life insurance. One option is to directly purchase it from an insurance company. Alternatively, you can opt for an independent local insurance agent or choose to go through an independent online broker.

It is crucial to emphasize the significance of obtaining life insurance through an independent broker, regardless of whether they are local or online. Agents who exclusively represent a single insurance carrier, like MetLife or John Hancock, may be focused on selling you a policy. While both companies are well-established and reputable insurers, navigating life insurance pricing can be exceptionally intricate. Failure to compare options could result in paying more than necessary.

When seeking guidance on life insurance, turning to an independent insurance agent whom you trust can be a good starting point. However, be prepared for the possibility of being presented with various life insurance options, which can be overwhelming. Personally, I found it helpful to determine my preference for level term insurance before delving into the shopping process.

Once you have identified the type of life insurance that suits your needs, comparing policies becomes somewhat simpler, albeit with several variables to consider. This is where the internet proves to be a valuable resource, as we will explore shortly.

What kind of life insurance to buy

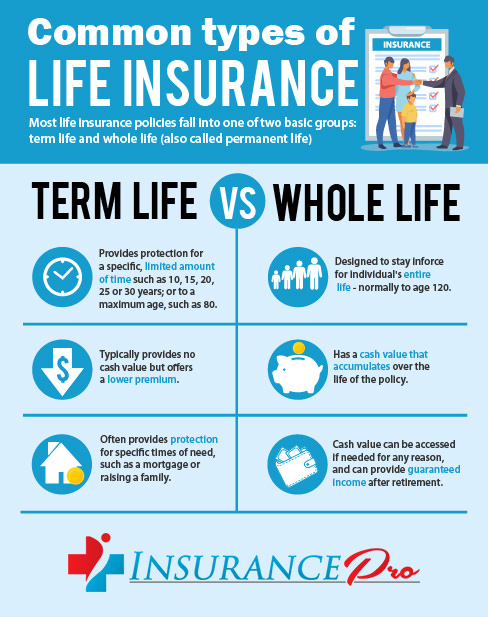

Term life insurance is the way to go! It’s not only cheaper, but for 99% of folks, it’s the smartest financial move when getting life insurance. Forget about whole life or universal life – stick with term life! It’s as simple as your car or home insurance. Pay your premium, stay covered. If the unexpected happens during the term, you’re protected. And the best part? It’s budget-friendly! Picture this: a healthy 20-something scoring a $1 million 20-year term policy for just $500 a year. Even a $250,000 policy could be as low as $15 a month!

Factors to consider when buy life insurance

When it comes to life insurance, there are several factors to consider. One of the most important decisions is what type of life insurance policy to purchase. With so many options available, it can be overwhelming to know which one is the right choice for you. Thankfully, the internet offers a wealth of information that can help you make an informed decision.

Among all the different types of life insurance, term life insurance stands out as a popular and practical choice for the majority of people. This type of policy provides coverage for a specified period or “term”, typically 10-30 years. It’s known for its affordability and simplicity – much like your car or home insurance.

Why should buy life insurance

So why should you choose term life insurance over other options like whole life or universal life insurance? One of the main reasons is cost. Term life insurance policies have lower premiums compared to permanent life insurance policies, making it a more budget-friendly option. This is especially beneficial for young families or individuals who are just starting out in their careers and may not have a lot of extra income to spare.

Another advantage of term life insurance is its flexibility. Unlike permanent policies, term life insurance allows you to choose the length of coverage that best fits your needs, whether it’s 10 years, 20 years, or even up to 30 years. This gives you the freedom to tailor your policy according to your specific financial goals and obligations.

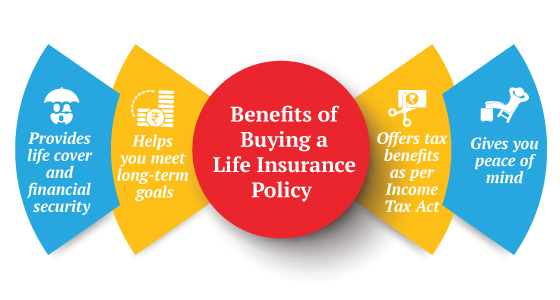

Additionally, term life insurance provides peace of mind knowing that your loved ones will be financially protected in case of your untimely death. It can help cover expenses such as mortgage payments, college tuition for your children, and other daily living costs that your family may struggle with without your income.

However, it’s important to note that term life insurance does not have any cash value accumulation like permanent policies do. This means that once the term expires, you will not receive any money back from the premiums you paid. But for many individuals, this trade-off is worth it in order to have affordable and flexible coverage during their working years.

It’s also important to regularly review and update your term life insurance policy as your circumstances change. For example, if you get married or have children, you may want to increase your coverage amount to provide more financial support for your loved ones in the event of your passing.

Additionally, some term life insurance policies offer the option to convert to a permanent policy at the end of the term. This can be beneficial if you decide that you want to continue having life insurance coverage after the initial term expires.

Overall, term life insurance is a valuable tool for providing financial protection for your family in case of your untimely death. It’s affordable and customizable, making it accessible for individuals at any stage of life. Consider exploring this type of coverage to ensure that your loved ones are taken care of no matter what happens.

Where to get online life insurance quotes

1. https://viralblogspost.com/archive/2277/

2. https://viralblogspost.com/archive/3462/

3. https://viralblogspost.com/archive/2428/

We recommend Policygenius because they provide more accurate quotes, let you complete more of your application online, and won’t harass you with telemarketing calls.

As insurance industry veterans, Policygenius designed their site to address the most inefficient and inconvenient aspects of buying life insurance.

Policygenius provides a thorough, yet easy, online form that returns term life insurance quotes. The price quotes you got online from most sites, in seconds, are rough estimates at best. According to Policygenius, however, 92% of their estimates are within $10 of a user’s actual yearly payment!

Better yet, Policygenius will only call you if you want to be called. Life insurance salespeople have a reputation for being aggressive with a capital A. As a result, after you request a quote from some other websites, they will call you multiple times a day for weeks.

I know because I tried it! Trust me, Policygenius provides a more pleasant experience; you can read more about Policygenius in our full review.

Information you need to get your quote

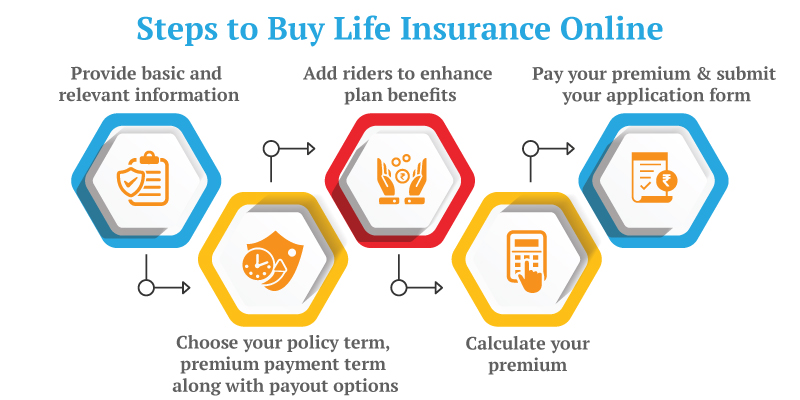

You won’t need any specific documents to get a life insurance quote, but you should be familiar with your medical history and the results of your most recent physical exam.

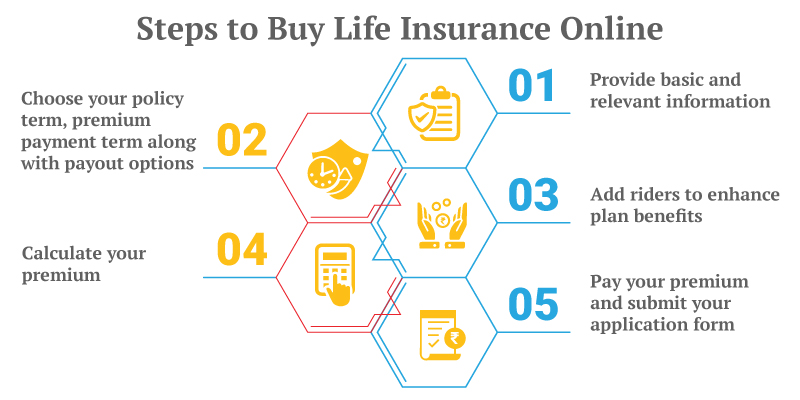

Here are the rough steps involved in comparison shopping for life insurance:

You’ll complete a brief form about you

Gender, age, weight, and whether you smoke are all questions you should be prepared to answer. Smoking is the biggest factor in pricing life insurance. Prepare to pay double if you smoke.

Most sites will require an email address and phone number before spitting back some quotes. But, again, not Policygenius.

If you want to compare life insurance quotes, the broker will ask a lot of personal medical questions, which is unfortunately necessary to provide accurate estimates. Be honest, as much of this information will be verified with your medical record or during a medical exam when you apply for insurance.

Select how much insurance you need (and for how long)

You need life insurance to replace your income in the event of your death, in order to provide for your family. It’s common to buy enough life insurance to replace your after-tax income until your children turn 18, plus an additional amount to cover education expenses or debts.

Common terms are 10, 20, and 30 years. If you’re not sure, use our easy life insurance calculator to find out how much life insurance you should buy.

You may be surprised to see a wide range of prices from different insurers

But without a more detailed application, most of these numbers are just guesses. Insurance companies employ actuaries who do nothing but crunch numbers to determine how to price insurance. The more information you provide upfront, the more accurate your quotes will be.

Learn your class: preferred, super-preferred, standard, or substandard

The insurance industry uses these broad groups to classify customers by risk. For example, if you are perfectly healthy, have a low body mass index (BMI), and do not have other risk factors (like smoking, dangerous activities, or a lousy driving record), you may meet the super-preferred class. By contrast, somebody who is overweight and has high blood pressure may only classify for the standard class and will pay more for the same insurance.

Although life insurance classes can provide broad guidelines of what you can expect to pay, every insurer works differently. For example, let’s say you have a hobby that insurance companies consider high risk – like flying a plane or rock climbing. Some insurance companies may place you in a lower class and charge you more for these “high-risk” activities. Another insurance company may insure you in a higher class, but place exclusions on your policy meaning you won’t receive a benefit if you die as a result of those activities.

Compare quotes from over a dozen insurance carriers

How to apply for a life insurance policy

After you’ve found your best quote, you’ll need to apply for the life insurance policy – this process can take several weeks.

The process of applying for life insurance can involve even more extremely personal questions, paperwork, and a medical exam.

Policygenius helps you get started, but you still have to buy insurance from an insurance company, most of which are still living in the pre-digital era. So, you can’t really buy life insurance entirely online.

1. https://viralblogspost.com/archive/3445/

2. https://viralblogspost.com/archive/2277/

3. https://viralblogspost.com/archive/2588/

Here’s what happens after you apply:

Verify your application

First, you’ll need to speak with an agent on the phone who will verify some of the information you provided online and confirm that the quote you selected is the best policy for you. The agent will then provide some paperwork for you to sign and submit your application to the insurer.

Schedule your medical exam

If the insurance company requires a medical exam (and most do), a contractor known as a paramedical professional will contact you to schedule the exam. The paramedical professional is trained like a nurse in performing a physical exam.

Policygenius, however, has partnered with Brighthouse SimplySelect℠ to offer term life insurance with no medical exam or lab work required! All you have to do is answer a few questions and talk with a Policygenius agent over the phone.

This significantly speeds up the underwriting process, so you can get life insurance in as little as three of four days, rather than a few weeks or months. And what’s even better is this doesn’t raise the premiums that typically come with no-medical exam policies.

Complete your exam, then wait!

The examiner will take a thorough medical history to confirm the info in your application. He or she will take your blood pressure and draw a blood sample that will be sent to a lab to test for cholesterol and glucose levels, tobacco and drug use, and diseases. These results will be shared with you by mail.

In life insurance applications, honesty is paramount: don’t be surprised if you must answer the same question about your medical history or tobacco use five times, but always answer honestly. Insurance companies share information, so misrepresenting information might not just get you denied from one carrier, but banned from many. Worse, it could give the insurer legal grounds to deny your family’s claim if you die.

The insurance underwriter’s job is to take all the information from your application and medical exam and decide whether to insure you and how much to charge. This takes many weeks. You’ll want to ask your agent whether the carrier binds any life insurance upon receipt of the application. For example, when you submit your application and a check for your first premium, many carriers will insure you for something, although not the full amount you’re requesting, pending completion of the underwriting process.

What to expect after you apply

When your policy is approved, it is placed in force and you will be notified, and receive a full copy of the policy.

If you didn’t already provide your agent with a deposit, you’ll be asked to make the first premium payment.

Some insurers may allow you to make your first payment to bind your policy upon submission of your application (prior to your medical exam). The insurer reserves the right to cancel the policy or increase your premium if your exam reveals previously undisclosed medical conditions, however.

Either way, be sure to ask when your policy will be effective – especially if you’re replacing an existing policy. Don’t cancel the old life insurance before you’re sure the new policy is in effect!

The agent will send you a hard copy of the policy. You should make a copy of this policy, place the original and the copy in different spots for safekeeping, and tell your spouse where they are. Finally, you can relax knowing that one of the most important pieces a solid financial plan is in place for you and your family.

That’s it! Although it seems like a lot, the process of buying life insurance can be easier than you think. Scheduling the medical exam and waiting on the results are the only real hassle.

Conclusion

Buying life insurance doesn’t have to be difficult anymore. Know that you’ll likely want term life insurance, not whole life insurance. And when looking for life insurance, aggregators like Policygenius can help you get quotes for term life in just minutes. Don’t wait any longer, protect your loved ones and secure their future by getting life insurance today on Policygenius.

In today’s fast-paced world, it is important to plan for the unexpected. One of the best ways to do this is by purchasing life insurance. Life insurance provides financial protection for your loved ones in the event of your untimely death. It can help cover expenses such as funeral costs, outstanding debts, and even provide an income for your family.

When it comes to buying life insurance, it may seem like a daunting task. However, with the help of online aggregators like Policygenius, the process can be much easier than you think. These tools allow you to compare quotes from multiple insurers in just minutes.